Скачать с ютуб Straight line depreciation в хорошем качестве

Straight line depreciation

1 год назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Straight line depreciation в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Straight line depreciation или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Straight line depreciation в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Straight line depreciation

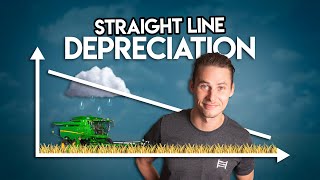

Straight line depreciation is a tried and tested method, which is used by some of the largest companies in the world, as well as your neighborhood grocery store. A short definition of depreciation is: the decrease in value of a tangible asset over time. The main idea of depreciation: buy a tangible asset (like a machine) now, then use and expense it over time. When you buy the machine, you put it on the balance sheet as an asset, something you own, as you expect to benefit from it for more than one year. Then in each of the years of usage, you take a piece of the asset from the balance sheet into the income statement as depreciation expense. In straight line depreciation, the size of that piece, in other words the amount of depreciation expense, is the same every year. ⏱️TIMESTAMPS⏱️ 00:00 Straight line depreciation 00:10 Definition of depreciation 00:50 Straight line depreciation graph 01:50 Depreciation expense formula 02:45 How to calculate depreciation expense 04:31 Depreciation journal entries 05:33 Depreciation levers in corporations 06:57 Extending useful life of assets Let’s have a look specifically at that straight line that is so important in straight line depreciation. The straight line runs from capitalized value on the left to residual value on the right. The capitalized value is the money spent by a business or organization to acquire or upgrade fixed assets, such as buildings, machines and equipment. Residual value is also known as salvage value, scrap value, or trade-in value. Residual value is the estimated value of the fixed asset at the end of its useful life. The straight line in the graph represents net book value, which is the capitalized value minus the sum of the depreciation expense over the history of using the asset. In the straight line method, depreciation expense is the same amount every year. In this example, we go from capitalized value to residual value in four equal steps. The depreciation expense formula helps you calculate the depreciation expense. In the numerator, calculate the total amount to be depreciated: the capitalized value minus the residual value. In the denominator, input the estimated useful life. Let’s discuss each of these terms. Capitalized value is any cost incurred to acquire, transport and prepare the asset for its intended use. The capitalized value can include shipping and installation costs. Residual value is the estimated value of a fixed asset at the end of its useful life. Try to support your estimate by solid data, rather than it being a wild guess. The estimated useful life is the number of years that an item is estimated to function when installed new, and assuming routine maintenance is practiced. How to calculate depreciation expense? Let’s feed the numbers from the example into the depreciation expense formula. With a capitalized value of $100,000, and a residual value of $20,000, the amount to be depreciated is $80,000. If the estimated useful life is 4 years, then the annual depreciation expense is $20,000 per year. If you want to record depreciation expense on a monthly basis, then simply divide that number by 12. There are two ways to put the $20,000 #depreciation expense per year into perspective: it is 20% of the original capitalized value of $100,000, or 25% of the depreciable amount of $80,000. The journal entries for straight line depreciation in #depreciationaccounting are as follows. When buying the asset: debit fixed assets on the balance sheet for $100,000, credit cash on the balance sheet for $100,000. When recording the annual depreciation expense, debit depreciation expense in the income statement for $20,000, and credit accumulated depreciation on the balance sheet of $20,000. Accumulated Depreciation is the title of the contra asset account on the balance sheet which is used when depreciation expense is recorded each accounting period. The accumulated depreciation amount on the balance sheet keeps growing over the years, all the way to the point that the fixed asset is fully depreciated, or the point where you reach the residual value. Net Book Value equals Gross Book Value minus Accumulated Depreciation. In our example, $80,000 at the end of year 1, $60,000 at the end of year 2, and so on. Philip de Vroe (The Finance Storyteller) aims to make accounting, finance and investing enjoyable and easier to understand. Learn the business and accounting vocabulary to join the conversation with your CEO at your company. Understand how financial statements work in order to make better investing decisions. Philip delivers #financetraining in various formats: YouTube videos, livestreams, classroom sessions, and webinars. Connect with me through Linked In! Want to get access to bonus content, and/or express your gratitude by buying me a cup of tea? Join my channel as a member through / @thefinancestoryteller

Comments