Скачать с ютуб Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel в хорошем качестве

Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel

4 года назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Parametric VaR and CVaR (Gaussian/Normal Distribution) in Excel

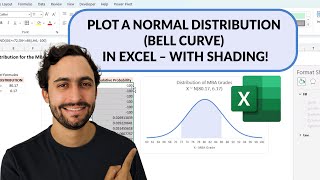

☕ Like the content? Support this channel by buying me a coffee at https://www.buymeacoffee.com/riskmaestro This is Part 2 of a 3-part series on Value-at-Risk (VaR) and Conditional Value-at-Risk (CVaR). If you have not watched Part 1, watch it first: • Historical Value-at-Risk (VaR) and Co... In this video, we will estimate the parametric VaR and CVaR, which means we have to assume a statistical distribution for the returns, in which I am using the Gaussian distribution (or Normal distribution), one of the more typically selected one. More resources on financial modeling on www.fabianmoa.com #FinancialModel #ValueAtRisk #ConditionalVaR #Netflix

Comments