Скачать с ютуб This is How to Specify ARDL Models в хорошем качестве

This is How to Specify ARDL Models

6 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок This is How to Specify ARDL Models в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно This is How to Specify ARDL Models или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон This is How to Specify ARDL Models в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

This is How to Specify ARDL Models

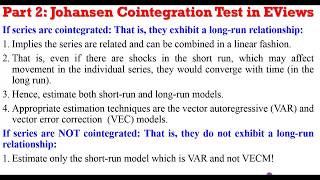

Upon performing the bounds cointegration test, there are two (2) likely outcomes: either the variables are cointegrated or they are not. If the variables are not cointegrated, the next thing to do is to specify the short-run model, which is the autoregressive distributed lag (ARDL) model but if cointegration is the outcome, then the appropriate model to specify is the error or vector error correction model (ECM/VECM) as the case may be. This video details the different model specifications under the ARDL framework. Follow up with soft-notes and updates from CrunchEconometrix: Website: http://cruncheconometrix.com.ng Blog: https://cruncheconometrix.blogspot.co... Forum: http://cruncheconometrix.com.ng/blog/... Facebook: / cruncheconometrix YouTube Custom URL: / cruncheconometrix Stata Videos Playlist: • (Stata13):Estimate and Interpret Two-... EViews Videos Playlist: • (EViews10):Interpret VECM, Forecast E...

Comments