Скачать с ютуб Forward rates are implied by zero rates (FRM T3-11) в хорошем качестве

Forward rates are implied by zero rates (FRM T3-11)

6 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Forward rates are implied by zero rates (FRM T3-11) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Forward rates are implied by zero rates (FRM T3-11) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Forward rates are implied by zero rates (FRM T3-11) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Forward rates are implied by zero rates (FRM T3-11)

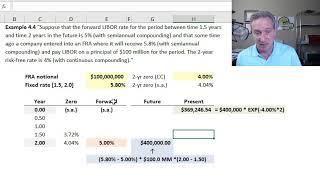

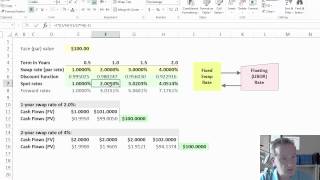

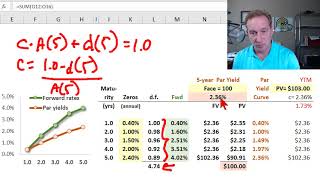

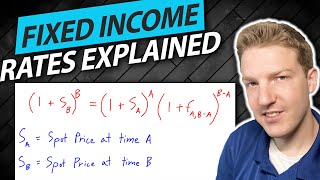

[my xls is here https://trtl.bz/2HMQkUU] Forward rates link two zero (aka, spot) rates by ensuring your expected return is the same between two choices: (1) invest at the longer-term spot rate versus (2) invest at the shorter-term spot rate and "roll over" into the implied forward rate. This is an implied forward rate that ignores other factors such as liquidity preference. Discuss here in our FRM forum: https://trtl.bz/2VH93eY.

Comments