Скачать с ютуб Option theta (FRM T4-18) в хорошем качестве

Option theta (FRM T4-18)

5 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Option theta (FRM T4-18) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Option theta (FRM T4-18) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Option theta (FRM T4-18) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Option theta (FRM T4-18)

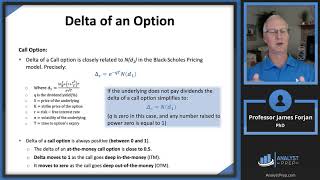

[my xls is here https://trtl.bz/2VKKgT1] Option theta (Θ) is the rate of change of the option's value with respect to the passage of time; it is a measure of time decay. The pure derivative returns theta in dollars per one year, such that it is common to divide by 250 (trading days) or 365 (calendar days). Theta is naturally negative; i.e., ceteris paribus an option's value decreases as maturity approaches. However, there are two exceptions: a deeply in-the-money-call with a high dividend yield (similarly a call currency option because the foreign interest rate is effectively a dividend); or a deeply in-the-money put on a non-dividend-paying asset. For an at-the-money option, theta "increases" (ie, becomes more negative) as maturity approaches. Finally, the theta of a put, compared to the equivalent (same strike and maturity) call option, is exactly greater by r*K*exp(-rT). Discuss this video here in our FRM forum: https://trtl.bz/30AivQ6

Comments