Скачать с ютуб Volatility (FRM Part 1 2023 – Book 2 – Chapter 14) в хорошем качестве

Volatility (FRM Part 1 2023 – Book 2 – Chapter 14)

5 лет назад

Скачать бесплатно и смотреть ютуб-видео без блокировок Volatility (FRM Part 1 2023 – Book 2 – Chapter 14) в качестве 4к (2к / 1080p)

У нас вы можете посмотреть бесплатно Volatility (FRM Part 1 2023 – Book 2 – Chapter 14) или скачать в максимальном доступном качестве, которое было загружено на ютуб. Для скачивания выберите вариант из формы ниже:

Загрузить музыку / рингтон Volatility (FRM Part 1 2023 – Book 2 – Chapter 14) в формате MP3:

Если кнопки скачивания не

загрузились

НАЖМИТЕ ЗДЕСЬ или обновите страницу

Если возникают проблемы со скачиванием, пожалуйста напишите в поддержку по адресу внизу

страницы.

Спасибо за использование сервиса savevideohd.ru

Volatility (FRM Part 1 2023 – Book 2 – Chapter 14)

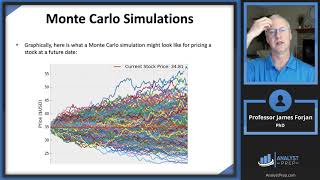

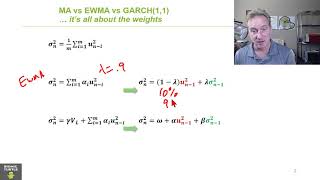

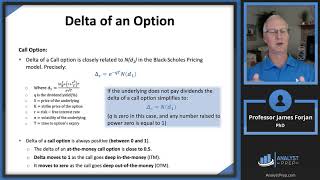

For FRM (Part I & Part II) video lessons, study notes, question banks, mock exams, and formula sheets covering all chapters of the FRM syllabus, click on the following link: https://analystprep.com/shop/unlimite... AnalystPrep is a GARP-Approved Exam Preparation Provider for FRM Exams After completing this reading you should be able to: - Define and distinguish between volatility, variance rate, and implied volatility. - Describe the power law. - Explain how various weighting schemes can be used in estimating volatility. - Apply the exponentially weighted moving average (EWMA) model to estimate volatility. - Describe the generalized autoregressive conditional heteroskedasticity (GARCH(p,q)) model for estimating volatility and its properties. - Calculate volatility using the GARCH(1,1) model. - Explain mean reversion and how it is captured in the GARCH(1,1) model. - Explain the weights in the EWMA and GARCH(1,1) models. - Explain how GARCH models perform in volatility forecasting. - Describe the volatility term structure and the impact of volatility changes. 0:00 Introduction 0:46 Learning Objectives 1:16 What is Volatility? 4:35 The Power Law 7:46 Weighting Schemes 8:40 The Exponentially Weighted Moving Average (EWMA) Model 10:16 GARCH (1, 1) Model 12:43 Mean Reversion 13:21 Forecasting Performance

Comments